Has the proliferation of free, ad-supported streaming TV delivered genuine, sustainable revenues for library owners, or are these channels reaching saturation point and following the same trajectory as linear TV?

Free, ad-supported streaming TV (FAST) was the buzz of the business three years ago as the shockwaves of the great ‘Netflix correction’ reverberated across the industry.

In April 2022, the world’s previously unassailable subscription video-on-demand (SVoD) market leader revealed a surprise plunge in customer numbers and plans for the introduction of advertising – a veritable Copernican turn for a company previously opposed to such a move.

Advocates of the ad-supported VoD (AVoD) model and those of FAST channels felt vindicated – players like Pluto TV, acquired by Paramount Global predecessor Viacom for US$340m in 2018; Xumo, picked up by Comcast for over US$100m just ahead of the pandemic; Tubi, taken over by Fox Corporation for US$440m shortly after; and Roku, which bought mobile-first flop Quibi in January 2021 to bolster its own FAST line-up.

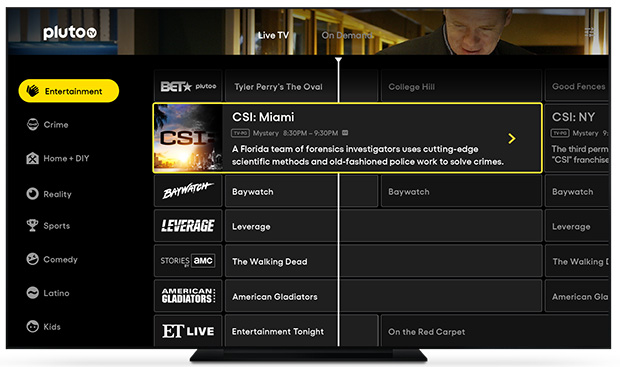

The data suggests FAST platforms like Pluto TV have maintained their momentum

The popularity of video streaming surged during this period as Disney+, Apple TV+, HBO Max and NBCUniversal’s Peacock all gained traction among holed-up households, with all, except the latter, following the Netflix playbook and launching with an emphasis on pay. But as Covid bubbles burst and the world emerged bleary-eyed, binge-view-sated and, in many cases, severely worse off, the attraction of SVoD plummeted and AVoD and FAST were the beneficiaries.

Amazon – better known for its Prime subscription service – rebranded its steadily growing ad-supported service IMDb TV as Freevee, while consumer electronics giants like Samsung, LG and Vizio (acquired by Walmart for US$2.3bn at the end of last year) beefed up proprietary platforms embedded within their connected TVs, featuring an expanding array of wholly owned and third-party FAST services.

FAST revenue grew almost 20 times between 2019 and 2022, reported UK research outfit Omdia in January 2023, predicting a further tripling between 2022 and 2027 to reach US$12bn globally. German data miner Statista put last year’s FAST market revenues above US$9bn and has this year predicted figures just shy of Omdia’s US$12bn for 2025, rising to over US$16bn by 2029.

Consumer take-up varies enormously depending on territory, with the once cable-dominated US embracing FAST first in parallel with cord-cutting. In 2018, some 10% of Americans – around 33 million people – regularly watched such channels, according to eMarketer. This year, those numbers rise to 34% of the population – close to 116 million viewers. What is notable, however, is that the outlook for the next three years suggests flattening demand, with an uptick to 35.8% of the US audience by 2028, or 125 million individuals.

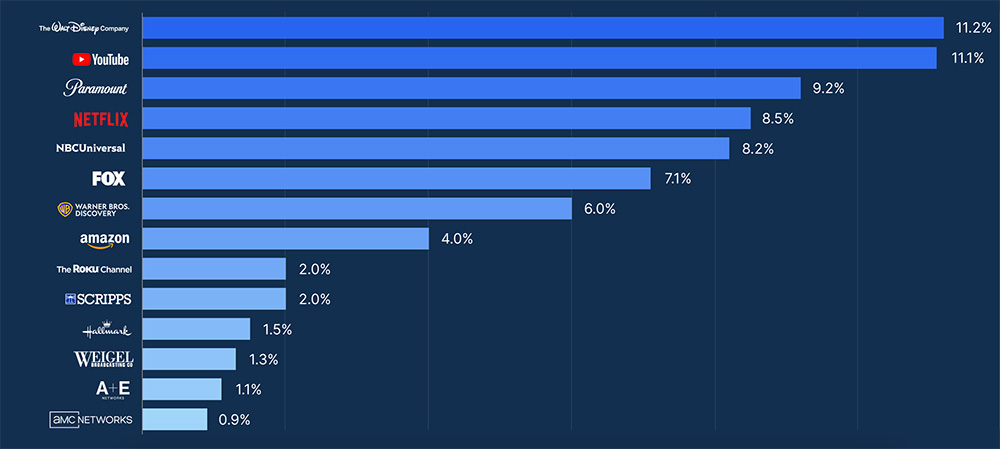

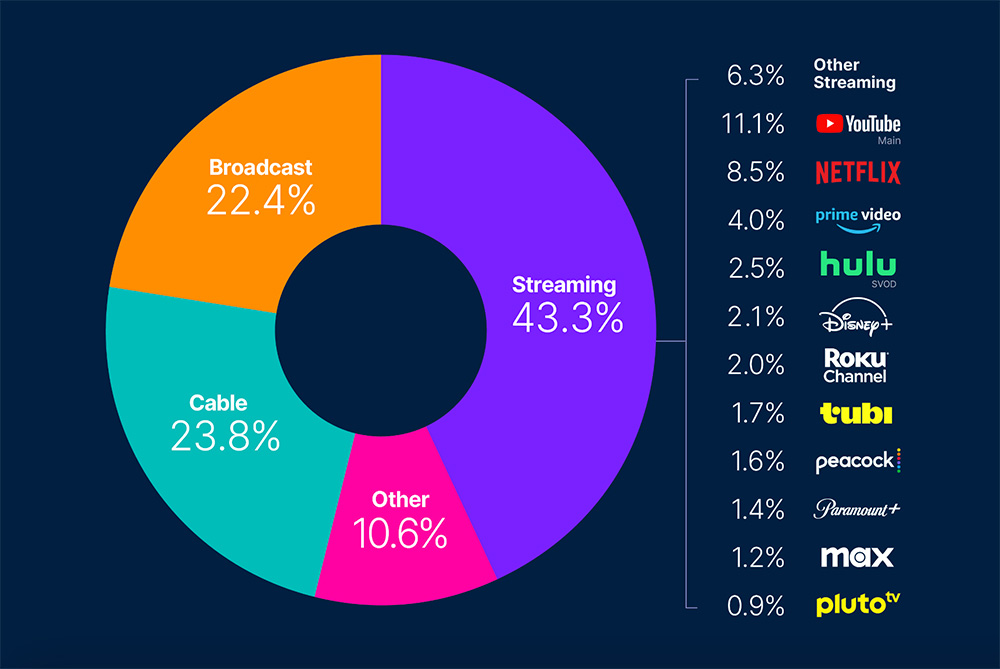

Nielsen Monthly TV viewing by distributor – December 2024

One of the pivotal stories of last year came in July when YouTube for the first time garnered more than 10% of all TV viewing stateside, with Netflix in fourth place behind Disney and NBCUniversal, based on aggregated figures for their respective streamers and numerous linear channels. Earlier in the year, in May, Nielsen noted continued momentum for FAST platforms Tubi, Roku Channel and Pluto TV, with a combined 4.1% share, noting Tubi usage rose 43% and Roku Channel 36% year-on-year. While the combined FAST share rose to 4.4% in July, this was outshone by YouTube’s symbolic 10.4%.

Fast-forward to December 2024 and YouTube boasted a record 11.1% of US TV viewing, with Netflix on 8.5% and the combined FAST figure at 4.6%, although it’s worth noting that this number only encompasses three of the myriad FAST platforms in the market. Samsung TV Plus, which has made a major push into the space over the past five years, is bundled into Nielsen’s ‘other’ category, presumably alongside the likes of Xumo Play, Vizio WatchFree+, LG Channels, Plex, TCLtv+ and more, which together had a total of 10.6%.

Last October, South Korean tech giant Samsung, for many years the global leader in connected TV sales, for the first time disclosed its own numbers, reporting 88 million monthly active users of Samsung TV Plus. It declared this was a rise of 50% year-on-year, with the US accounting for the lion’s share. Roku, meanwhile, reported more than 90 million streaming households, up from 85.5 million in October.

Nielsen Monthly TV viewing by platform – December 2024

Tubi said in January it had reached 97 million monthly active users, versus 78 million in May last year. Pluto, meanwhile, last reported 80 million monthly active users in May 2023, as Paramount Global began entertaining suitors. The service reputedly brings in over US$1bn annually but its future is an open question with the final structure of its parent’s merger with Skydance yet to be revealed.

All in, there were around 2,000 FAST channels available in the US and upwards of 5,000 globally last year, according to self-styled ‘FASTMaster’ Gavin Bridge, as content owners and licensors have seized on the opportunity. The likes of A+E Networks, All3Media, AMC Networks, Banijay, BBC Studios, Blue Ant Media, Cineverse, Electric Entertainment, FilmRise, Fremantle, Lionsgate, Sony, Warner Bros Discovery and more have inundated the sector with a cornucopia of genre-based and single-IP destinations – channels dedicated to series as varied as Baywatch, Top Gear, The Walking Dead, Mr Bean and Midsommer Murders.

But the conversation around FAST is changing. Bridge signalled as much before signing off as FASTMaster, ahead of starting a new role within Amazon MGM Studios’ as creative lead for the company’s FAST programming unit in July. His final ‘State of FAST’ report spoke of ‘peak FAST’ and referenced the US market’s maturation and slowing growth, underscoring, however, that it is continuing to expand.

Bridge also wrote of attrition rates, that is the number of FAST channels being culled as platforms refine their line-ups. At 2%, the drop-off rate doesn’t look too bad on a monthly basis, but the annual picture shows one-fifth of channels were extinguished in the year to June last year. UK research firm 3Vision puts the figure even higher for the year to August 2024, finding that 27% of channels were eliminated across all platforms in the US.

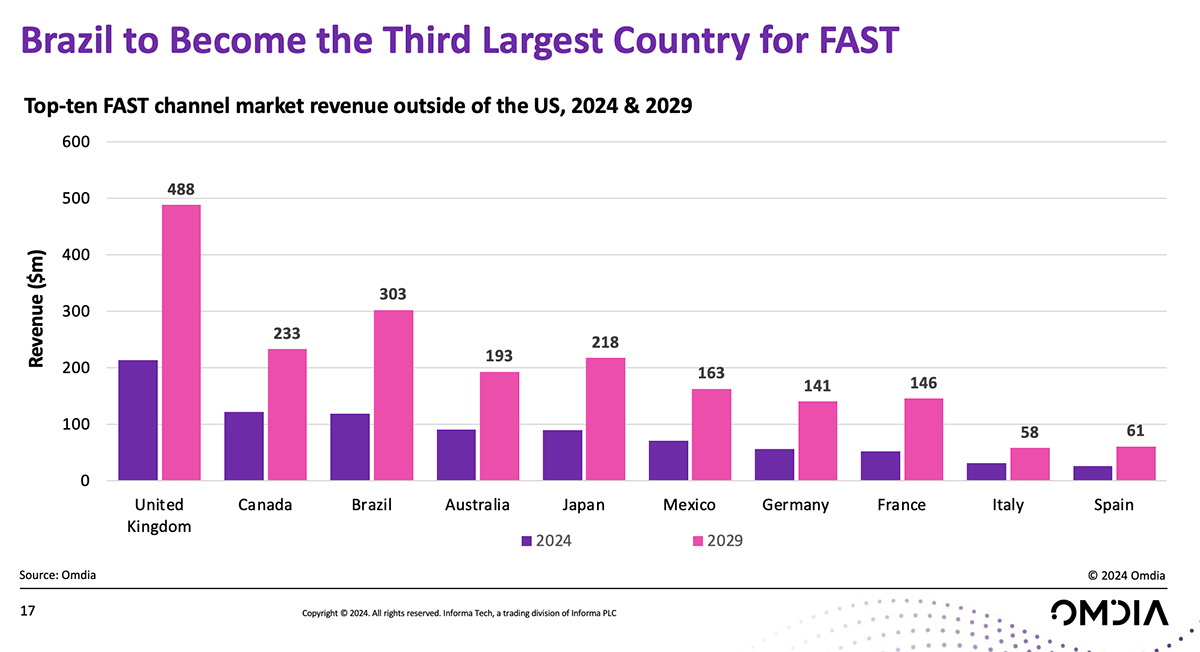

Elsewhere, the UK is currently second in terms of the number of FAST channels available (some 600) and revenues from them were pegged at just over US$200m last year by Omdia, with the figure set to rise to US$488m by 2029. While Canada currently comes next, topping US$120m in FAST revenue, increasing to US$233m by 2029, Brazil will leapfrog it by then, claiming the third spot with over US$300m. Australia, Japan and Mexico show reasonable gains, as do Germany and France from their present low penetration, but revenues in each will likely remain under US$150m in five years’ time, with Italy and Spain trailing further.

The UK and Germany are also showing signs of FAST market maturity, according to 3Vision, with over 30% of all channels being dropped by at least one major platform in each territory in the past year. These shifts have left some feeling sceptical about FAST’s long-term prospects.

“FAST is too overhyped by inflated forecasts that looked to reinvent the wheel in a streaming-led future,” says PP Foresight tech, media and telco analyst Paolo Pescatore. “For the most part, the user experience is still dreadful and usage is skewed towards folks leaving TVs on rather than actually watching. Unfortunately, I was not a believer in FAST. It felt like everyone in the media and broadcast industries was jumping on the bandwagon. But ultimately, who is making money from FAST? They are very few and far between.”

In contrast to other analysts that have focused on the sector’s growth story, Pescatore predicts FAST will “fall faster by the wayside” in 2025 and beyond, adding: “It might still play a small role in niche markets, but that’s it.”

He is not alone in his concerns. While S&P Global foresees annual FAST revenue of US$1bn across Europe by 2028, it notes that usage rates for platforms like Samsung TV Plus, Pluto TV and LG Channels ranged from about 2% to 8% across the UK, France and Germany last year, predicting revenue from FAST platforms in Europe will fall by 14% in 2025 – half the growth figure for 2024.

Samsung TV Plus has pushed into the FAST space over the past five years

“We did not expect the reach and revenues to stabilise so early in the development of this relatively new medium,” says Patrick Hoerl, MD of German factual producer and distributor Authentic, operator of six FAST channels spanning areas such as wildlife, travel, history and science.

“I can remember a time, maybe a year ago, when it was all about FAST and it seemed like the world would be ruled by FAST channels very soon, and that has changed recently,” he continues.

“There are many different voices about FAST and how successful it could be, and this is healthy. But nowadays we have new topics in the market, like AI, for example. It’s not a space that has found the ideal business model yet in terms of advertising sales, so we are still trying to figure that out.”

Hoerl emphasises that Autentic remains committed to FAST for the time being and doesn’t believe it has reached saturation point, but admits margins in the YouTube channels business, for example, are more attractive. Like Pescatore, he says major work needs to be done to improve the consumer friendliness of the FAST experience.

“A lot of channels were launched just to fill space in the early stages, and those channels that don’t meet immediate audience needs are now being replaced,” he says.

“It’s time to look at what audiences really want in terms of how specific should the positioning of a FAST channel be, which are the brands that are most appreciated in the FAST universe? Those questions weren’t asked at the early stages of the FAST development. The platforms were focused on the technology, where to get the content from and so on, and maybe during the first days of the medium, there was not enough attention on consumers.”

Katrina Kowalski

Katrina Kowalski, senior VP, international content programming and acquisitions at Pluto TV concedes these are good points, but naturally argues that FAST will be around for the long haul.

“This is not a fad, this is something that’s here to stay. More and more producers and content providers are realising this is not a replacement for what’s already in the ecosystem, but a really wonderful companion and another way you can monetise content,” she says.

“Monetisation is different in every market and there are a lot of variables at play. There is the size of the economy, the amount of ad inventory in the market, the ability of the sales team on the ground to sell direct versus programmatic versus sponsorship. The monetisation is driven by the impressions served, so it’s really important to understand that an impression is not served if somebody doesn’t watch your stuff. That is one of the critical pieces of the pie.”

With over 5,000 FAST channels available globally, and sometimes hundreds on each platform in each territory, visibility is indeed an issue, although some would say this was ever the problem since the days of cable and satellite – and more so 20 years on, after the arrival of YouTube.

Moves to trim some channels are part of this process and figures for attrition rates perhaps mask the fact that FAST is also ideally suited to easy-to-launch promotional pop-up channels that come and go. But the platforms insist they are working hard to improve the user experience and therefore, in theory, the returns for content partners.

Jennifer Batty

“We want to make sure that we’re launching the strongest channels to entertain somebody who has bought a Samsung device, and we want to make sure for our partners that their channels are going to have an audience,” says Jennifer Batty, Samsung TV Plus’s director of content partnerships for Europe and the Middle East.

“For us, it’s about discoverability. It’s about making sure that you can find the content you want to watch. Four or five years ago, it was slightly different because it was so new and nobody really knew what FAST was or what FAST was going to become. But now we look at what is that audience, what is the local feel, what are we looking to achieve with that channel?

“When we first started, it was very simple: ‘Here we go, here’s a channel, a very basic revenue-share business model. Every month, here’s your remittance. Thank you,’” continues Batty. “As it’s evolved, we’re out licensing individual titles just like any other broadcaster, creating a grid, scheduling the channels. We now look at different partnership models.”

The company struck a major deal with Amazon last year to become the exclusive FAST home for season one of big-budget JRR Tolkien drama The Lord of the Rings: The Rings of Power. Although in place for only a limited period ahead of the season two premiere on Prime, the alliance highlighted this changing approach.

As 3Vision senior analyst Jed Ayloff points out, it was particularly interesting that the series was not available on Amazon’s own platform, Freevee. “This suggests a deliberate strategy to balance revenue generation through a second-window exploitation with Samsung while also using FAST as a promotional tool for the new season premiering on SVoD,” he says.

In some ways, of course, this is preaching to the converted. Amazon, from its own experience, clearly has an understanding of the power of FAST but the broader advertising market still requires some persuasion, and the availability of big-name TV shows and movies gives platforms greater credibility.

“We have content like BBC Earth, we’ve had Narcos, we’ve had Mad Men, Schitt’s Creek – we’ve put some of the biggest IPs out globally now within the Samsung TV Plus environment, so it’s really about how we educate advertisers looking for a connected TV audience,” says Batty. “They don’t want that YouTube audience. They’re looking for something that is a little bit more targeted and, with Samsung, one of the benefits we have is that we own the screen, we own the glass.”

The firm touted its 300 million Samsung TV and Galaxy device owners in the US, Canada, Brazil, UK and Germany in the Rings of Power announcement and, according to Omdia, the firm is on track to generate US$3bn of revenue from connected TV advertising by 2029 – more than double last year’s figure of US$1.4bn.

Batty says Samsung can give brands something that few others are able to offer. “When you turn your TV on, the very first thing that you see is an ad that takes over the entire screen, which then, from an advertiser’s point of view, gives them multiple touch points from that native ad all the way through to a traditional 30- or 60-second spot across the 150, 200 channels that we have.”

It is perhaps a subtle change in framing the FAST debate, broadening the conversation under the connected TV (CTV) catch-all umbrella. Indeed, Omdia carves this out now as a separate research topic, with a September report noting that hardware manufacturers, like Samsung, are increasingly capitalising on such platform revenues over hardware sales.

Roku, however, is at the forefront of the CTV advertising space, claims the analytics outfit, on track to generate US$5bn in revenues from it by 2029, spanning FAST, CTV user-interface ads and third-party inventory shares.

David Eilenberg

“The market for FAST still has room to run,” says Roku Media head of content David Eilenberg. “Television viewing in general is migrating to a streaming experience, so if you accept that’s a trend that hasn’t reached its peak yet, then naturally ad spend will follow from linear towards streaming. There is still upside in the business, even as it’s become more mature.

“One of the advantages of streaming, in terms of being able to accommodate both really broad FAST channels and more niche ones, is that it has discoverability tools that linear never quite did. Our job as a platform is to get the viewer to something that surprises and delights them and keeps them engaged, and this digital universe has more ways by which to do that. How much is too much? That’s an organisational and curation question, as opposed to ‘can streaming accommodate a nearly infinite amount of content?’ It can and does. If you look at YouTube, which is actually the biggest streaming app of them all now, that just proves the model, in a way.”

Eilenberg says conversations with the advertising world are advancing and this can only be a benefit, not only to Roku but its third-party FAST channel operators too.

“When you think about what streaming was even a few years ago, many of the best-known services had no engagement with advertisers whatsoever, and it was a subscription-only model. Now, I think every SVoD, save maybe Apple, has an ad tier, so you’re seeing the advertising community once again [being] central to how television is being produced – not just at Roku but across all of streaming,” he says.

“The presumption is that spend will follow engagement, so as engagement migrates holistically towards streaming, you’re going to see the spend continue to do the same. The other thing that’s interesting and exciting is seeing how the brands and media agencies are starting to think very deeply about how they support content and storytelling that speaks to their values. That’s something we think about quite a lot too.”

Content owners are also broadening the way in which they define success in the FAST environment. BBC Studios has been in the business since its inception, striking its first FAST partnership with Pluto TV in 2019.

“We’ve gone from having one platform partner in the US to 14, from having two FAST channels – Antiques Roadshow and Classic Doctor Who – to having 18, and another seven in EMEA and also recently expanded into Australia,” says Beth Anderson, senior VP and general manager of FAST channels and VoD sales for BBC Studios North America and Latin America.

Classic Doctor Who was one of BBC Studios’ first FAST channels in the US

Top Gear has since been added the list of single-IP outlets but it’s genre-based channels like BBC Earth, BBC Food and BBC Comedy that have really bolstered the portfolio, with the first proving particularly popular among manufacturers like Samsung, which are keen to use the power of BBC natural history programming to show off the power of their TV screens. Then there’s BritBox Mysteries, a FAST barker channel of sorts for BBC Studios’ BritBox SVoD service.

“We are seeing FAST as a really wonderful ‘top-of-funnel’ introduction for a lot of these brands,” says Anderson. “It’s very pertinent for the single-series IP channels that are there, but also it allows us to uncover new economic models across the entire media ecosystem.”

She notes that Antiques Roadshow returned to broadcast TV in the US after gaining traction on FAST, particularly among younger viewers introduced to the show, and indeed, linear TV for the first time. “We opened a massive door of exposure and started to see young people making TikTok videos about it, which was quite special.”

FAST, Anderson adds, was “never supposed to be a replacement business. It was always a complimentary one, and we’re not seeing any evidence of cannibalisation, which is important when we think about the future.

“Yes, absolutely, there’s always cost, but there’s significantly less cost in FAST than there is in broadcast TV and there isn’t that level of commitment to keep things going if they’re not working.

Graham Haigh

“If you think about this as its own silo, it’s going to get expensive really quickly, but the skills you’re getting and the lessons you’re learning from performance-based revenues are so impactful for the rest of the business you’re running, and can inform international strategy too.”

Graham Haigh is chief operating officer of Zoo55, a new division within ITV Studios (ITVS) established in October to bring together the company’s digital activities across social media, gaming and more, including FAST.

Having come to the latter market in 2022 with a Hell’s Kitchen channel in the US, ITVS now has a portfolio of 20, encompassing other single-IP outlets like Come Dine With Me, River Monsters, Ninja Warriors and, most recently, The Graham Norton Show, plus a range of genre-based destinations. It has others too, operated with third parties, such as an Agatha Christie Poirot & Miss Marple channel with Pluto TV in Spain, plus a movie channel called British Screen Classics, available in the UK via a pact with StudioCanal.

Haigh agrees with Anderson that the key to making the most of FAST is not to treat it as an isolated line item on the P&L, rather part of the overall business that brings sometimes tacit benefits.

“We’ve got multiple brands that have a significant presence in the social space, not just on YouTube but TikTok, Snap and Facebook. And to have hugely successful FAST channels, there’s different audiences for different platforms, and you need to think about those,” he says.

“A three-minute vertical video for Facebook Reels can deliver you significant revenue, but it takes a huge amount of skill to pick the right clip from The Graham Norton Show, for example, and edit and present it for that audience, and then in a different way for the audience watching on TikTok.

“YouTube is obviously pushing more towards connected TV viewing, so longer-form is more popular in that space. And then, in FAST, there’s a different audience watching The Graham Norton Show on Samsung TV Plus, Pluto or Roku, but you can use that content that you’ve expertly curated within that channel to essentially create more content out of the same show and present it in a different manner to a different audience. You can use that as interstitials and promos from a marketing point of view to other channels in your network, so there’s a multitude of skills that you’ve got within a team curating content on owned and operated channels that can be multi-purposed across the business.”

Shaun Keeble

Shaun Keeble, VP of digital distribution at Banijay Rights, agrees. “What we’re seeing here is and incremental revenue opportunity but also market awareness of a show that may not necessarily be actively in commission for traditional broadcast but entering a new platform with perhaps a younger audience to try to ignite excitement around that show – which can, of course, then lead to other opportunities,” he says.

Banijay has been in FAST since 2019 and has over 30 channels spanning programme brands such as Deal or No Deal, Fear Factor, Wipeout, MasterChef, Survivor and, most recently, the Mr Bean animated series.

“Eighty per cent of global revenue from FAST consumption is still coming from North America and connected TV advertising is now the number-two most demanded inventory in the US behind social media,” says Keeble, who backs up Omdia’s aforementioned findings, however, that markets such as Brazil are also beginning to offer notable returns. But again, he stresses that FAST should not be regarded as a standalone category.

“When we think about FAST channels, this is a product whereby of course we’re programming full-length episode content, and this is very similar to the strategy we’re adopting on YouTube, where we are seeing much better monetisation and minute stream growth through full-episode publishing. So you find yourself in a position where there are synergies and learnings from both, and in terms of monetisation opportunity, of course, YouTube is the second largest search engine across the globe.”

Haigh also draws parallels with the Google-owned platform, citing last year’s Nielsen stats about YouTube claiming the top spot on US TV screens as a pivotal moment.

“It feels like there’s been a sort of ‘click’ in people’s heads across the industry. There’s a recognition that this isn’t just a platform for influencers and creators but it’s also a bona fide, credible platform that can drive huge levels of viewing, of engagement and revenues. And, by working with them, there are some allowances in terms of being able to sell your own inventory and having a good degree of ownership about how your content is presented within that world.”

Zoo55 entered the FAST space in the US with Hell’s Kitchen

To some degree, these positives about YouTube hold up a mirror to FAST and find it, at least in some cases, wanting.

Haigh identifies monetisation as the primary challenge facing the space. While he says that having big-name IP like Hell’s Kitchen in the US works “exceptionally well,” content that doesn’t fall into that category struggles to break through in such a crowded marketplace. Elsewhere, the revenues can be elusive.

“We see, for example, some huge levels of viewing in Spain in terms of impressions driven but the monetisation does not stack up there, unfortunately. In Germany, there’s a little bit more symbiosis in the relationship between impressions and revenue but for the same number of impressions in the UK, in certain instances, we’re not seeing the same level of revenue,” says Haigh.

“That whole ad model and how the platforms – or even the content owners, if we choose to take some ownership of inventory – are able to monetise those impressions needs to improve.”

The exec would also like to see FAST platforms become more open with content partners in terms of information sharing. “Having that transparency of data, almost real time like you do on something like YouTube where you can be very reactive, it doesn’t quite exist in the FAST world,” says Haigh.

His final complaint, which he stresses does not apply to all purveyors of FAST, concerns presentation.

Roku reported more than 90 million streaming households

“The likes of Netflix, Disney+, ITVX and others have done a great job of making content look incredible on your TV and making the process of finding something and manoeuvring around the user interface very seamless. Some of the FAST platforms haven’t come from that content background necessarily, so they’re evolving how they present their ecosystems, and there’s still a way to go there.”

For Keeble, there are similar concerns. “As a content owner, you want to stand out,” he says. “From the perspective of working closely with the platforms, we have openly said, for many years, that we don’t intend to be a lean-back partner when it comes to our content offering. We want to offer a FAST channel and then continuously work with the platforms to make sure that the marketing and awareness of that channel is very prevalent, because we don’t want to be forgotten about.”

Returning to Autentic’s Hoerl, he believes as FAST evolves and the pressure to deliver long-term revenues grows, the platforms will increasingly focus on established IP.

“What’s becoming clear now is how important brands are in the FAST space. Without a strong brand – whether you have built it up yourself or whether you just adopted a single-IP channel made from a well-known brand – your protection level is very low,” says Hoerl.

“If you’re just a random collection of shows, you’re likely to be kicked out after a reasonably short period of time and be replaced by something that has a stronger immediate appeal to people. To build a brand from scratch on FAST is quite expensive, and I don’t know many people who would take that risk at this point.”

Hoerl believes the platforms need to go even further to prove their true worth. “Ultimately, the future of FAST channels will be decided by whether that medium will enable content makers to produce and finance originals. If it remains a medium that just does long-tail programmes that have long been written off or have been sitting in back-catalogues, that’s not going to be sustainable,” he says.