How Indian entertainment sector can capture $6bn in unrealised value by 2030

A report published today based on C21’s Content India Summit and research from Allied Global Marketing has highlighted a US$6bn opportunity for the Indian entertainment business, defined by increased international partnerships and a focus on revised content and operational strategies.

Titled The Future Of The Indian Entertainment Business In Partnership With The World, the report is based on the findings of the Content India Summit – a coproduction between DishTV and C21Media – which took place in Mumbai on April 1. That summit will inform a three-day Content India event being held in March 2026.

Image courtesy of Allied Global Marketing

Click to enlarge

The report suggests a number of key strategic and structural changes that could add US$6bn in value to the Indian entertainment business by 2030.

India is already one of the largest entertainment markets globally, but it dramatically underperforms relative to its full potential. Today, India’s 551 million OTT users generate only US$2.1bn in revenues, while comparably sized or smaller markets like South Korea export billions worth of content globally.

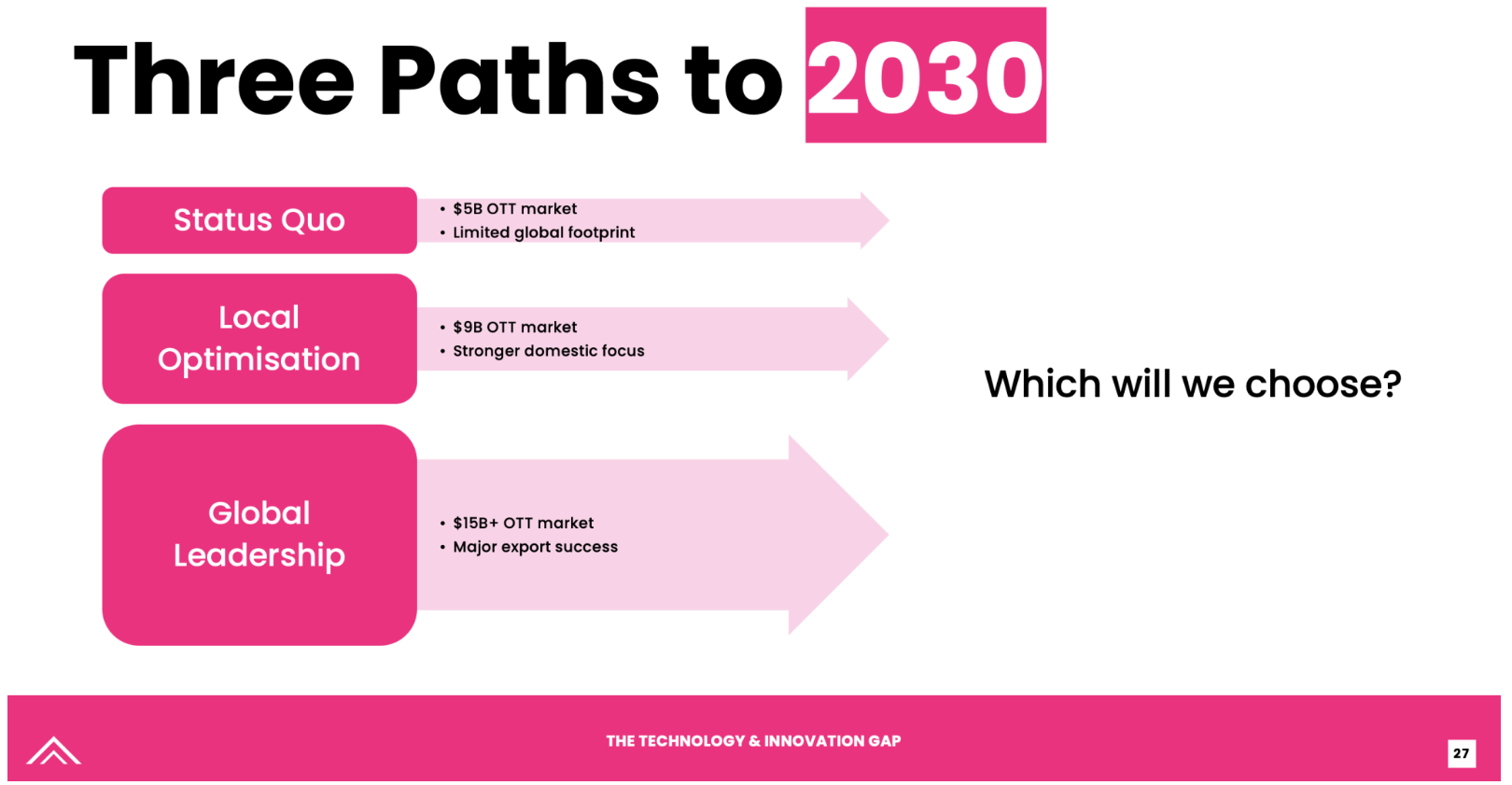

According to the report, if India stays on its current course, it could build a respectable US$5bn OTT market. Local optimisation efforts could stretch that to US$9bn.

But by embracing a bold strategy – repositioning globally, adopting cutting-edge technology and realigning content strategies – India could unlock a US$15bn-plus entertainment economy by 2030, becoming a major global soft power in the content business.

This was suggested by Jamie Crick of Allied Global Marketing in his opening address to the Content India Summit, and informed the core narrative of the one-day event.

Crick’s presentation, and the sessions that followed during the summit, defined how important global partnerships will become to stimulating growth in the market.

The report concludes priorities for change are:

• Creating new international partnerships around authentic Indian storytelling.

Inviting major studios to back a series of Indian pilots to define new global ambition.

• To reconcile Indian audience demand with content creation.

• To support and nurture the creator economy.

• To ensure India is at the heart of a new production revolution driven by technology – including AI.

• To recognise a new hybrid content economy is emerging and position the market to take full advantage.

• Define local content with distinct Indian flavour that can also export to the world.

Commenting on the report findings, DishTV MD Manoj Dopal said: “It is clear that the Indian entertainment business is a force to be reckoned with on the global stage. But it has the opportunity to make an even bigger impact globally by partnering with international players on its own terms. It is also ideally positioned to become a central hub for global production, with unrivalled resources, skills and locations.”

David Jenkinson, C21Media founder and report editor, said: “The world is changing fast. The emerging creator economy, the rise of AI tech and the opportunity to work together across borders is set to reshape the global entertainment business. As this report shows, India can be at the heart of that. Of course, there are many challenges. But they are all addressable and the upside is significant for all.”

The report notes a number of issues blocking India’s full potential:

1. A mismatch between audience demand and content production

• Comedy is the most preferred genre (nearly 30% of audience preference) but only 10% of premium content produced is comedy.

• Drama, crime and thrillers dominate production (60% of new releases), misaligned with what audiences want.

• Local, culturally authentic content is overwhelmingly preferred (86% of premium OTT viewership).

The learning from this is that India should produce more authentic, relatable, lighter content aligned to mass tastes – not just prestige dramas. Authenticity drives both domestic success and international breakout hits like RRR.

2. A misunderstanding of the dominant viewing experience

• Despite perceptions of India as mobile-first, connected TV viewing is surging:

– YouTube connected TV usage quadrupled from 2022 to 2024.

– Family co-viewing at dinner time is normal.

• Content still heavily targets urban, individualistic mobile users, leaving rural and family viewers underserved.

• Ninety-two percent of India’s online video minutes are spent on YouTube, not premium OTT.

• YouTube’s strength:

– Creator-driven

– Shortform

– Hyper-relevant

The learning from this is that Indian entertainment needs to embrace family-friendly co-viewing formats and leverage creator ecosystems and snackable content styles for OTT platforms.

3. The global opportunity gap

• Success stories like South Korea (Hallyu wave) and Spain (Money Heist) show that local authenticity and universal themes drive massive global success.

• Indian success stories (RRR, Pathaan, Kantara, KGF 2) show this works domestically and internationally.

• But most Indian content exports are exceptions, not the rule.

• Global streamers are recalibrating: profitability over subscriber growth.

The report also suggests new growth drivers for the next decade:

1. Become the global production partner of choice

• Cost advantage:

– Indian premium series = US$1m-2m/episode.

– US/UK = US$5m-15m/episode.

• Global slowdown:

– South Korea’s entertainment industry is contracting.

– US and global studios need affordable production hubs.

• AI-driven cost reductions:

– OpenAI API costs fell 80% in two years.

– Virtual production can cut costs by over 30%.

The learning from this is to position India as the most cost-effective, tech-savvy content production partner.

2. Harness the global diaspora

• Thirty-five million affluent Indian diaspora consumers abroad – a vastly underleveraged audience.

• Until now, diaspora-focused content has been mostly nostalgic.

• Opportunity: Broaden genres – action, thrillers, sci-fi – to appeal both to diaspora and mainstream global audiences.

The learning from this is to target the global diaspora as a strategic bridge to mainstream global success.

3. Leverage advanced technology

• Only 24% of Indian studios use AI tools, vs. 76% of US studios.

• Virtual production, AI workflows, automated localisation (dubbed/subtitled faster) are essential to compete.

• Example:

– Digikore Studios cuts post-production time by 40% using AI.

– IPL innovations (Hype Feed, Watch Parties) show India’s tech capabilities when strategically deployed.

The report concludes that India has the creativity, technical talent, cost advantage and audience size to become one of the top three global entertainment powerhouses in the next decade. But execution – not just ambition – will determine whether it captures the US$6bn in unrealised value sitting on the table.

It recommends that Content India 2026 and related initiatives must push toward:

• Urgent action.

• Strategic partnerships (local and global).

• Smart technology adoption.

• Authentic, emotionally resonant storytelling

• Institutional and regulatory support for long-term global expansion.

“The future of Indian entertainment will not be gifted. It must be built,” concludes the report.

The Future Of The Indian Entertainment Business In Partnership With The World is published by DishTV and C21Media and is a Content India initiative. The report also includes the Content India Summit session videos, which contributed to the report findings.

You can see the list of contributors by CLICKING HERE.